What efficiency means for personal finance

Searching for the Pareto Frontier of financial paths

At the end of my last post, I mentioned that Syrplus does not aim to promote any particular sort of lifestyle. If you want to be hyper frugal and reclaim some of your life from The Corporate World by retiring early, do it. If you want to work super hard and yeet the money on sportscars and vacations, do that. Most people’s goals probably fall somewhere in the middle.

What Syrplus does aim to do is help people be efficient, whatever their financial goals may be. In this post, I’d like to better explain what is meant by “efficient” in this context.

From a very high-altitude view of personal finance, there are fundamentally two optimizations we should be considering:

Work less (that is, have less work required of you)

You could argue that there should be a third item called “Lower risk,” but per the Trinity Study method of encapsulating risk, we’re already only considering financial paths that are considered to be appropriately risk-averse. For more on this, read our first blog post:

We can compare different financial paths along these two axes. All else equal, the sooner one can stop working the better. Similarly, all else equal, the higher spending allowance the better. If a financial path is worse than another along both axes, it is not worth considering. ←This is the critical point here.

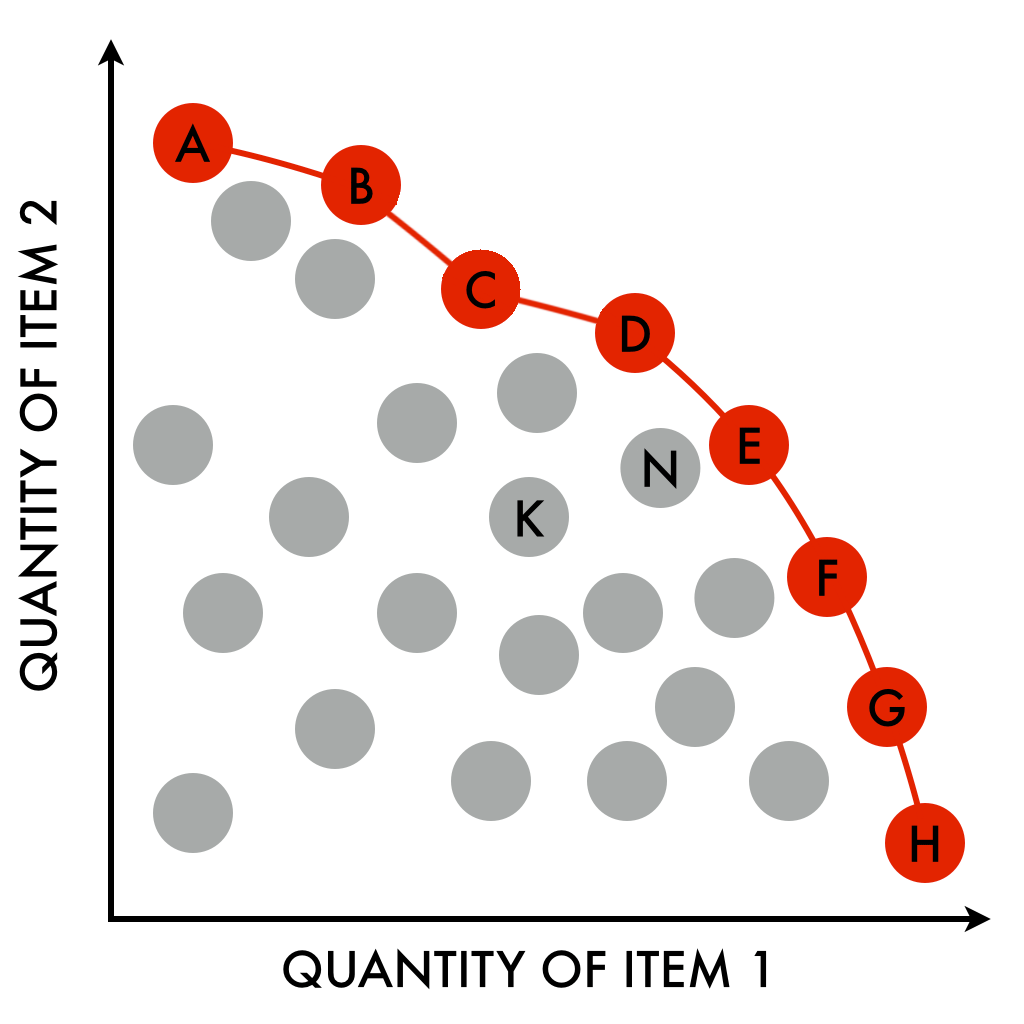

With this, let me introduce a helpful concept known as the Pareto Frontier. When comparing items along two axes, the Pareto Frontier is what remains after the removal of any item that is strictly worse than some other item. Items on the frontier are said to be Pareto Efficient. The plot below was taken from the Wikipedia page on the Pareto Frontier. For our purposes, it is helpful to think of the axes as “desirability according to quality 1” vs “desirability according to quality 2.”

For an excellent explanation of Pareto Efficiency, check out this blog post written by Erik Bernhardsson.

What we want is to uncover financial paths that are on the Pareto Frontier according to the axes I mentioned above. This frontier is the spectrum between the two lifestyles I mentioned at the top of this post. The hyper-frugal person is on one axis and the work-hard/play-hard person is on the other.

Each of the interior points represents a financial path for which one or both of the following is/are true:

the person could have retired earlier without spending less

the person could have spent more without retiring later

A lot of the financial mechanisms we utilize serve to make us more Pareto Efficient. For an example of a path that is extremely inefficient, imagine somebody simply foregoing all retirement/investment mechanisms and planning to retire on cash alone. This person is clearly not on the frontier.

You wanna be on the frontier.

Thanks so much for reading. Please consider trying out Syrplus for free by signing up on our website:

If you dig this post, share it somewhere cool!

Recently I saw somebody on Twitter saying that their goal was to keep their spending as low as possible, and do what they can to avoid their spending rising with inflation. I also pretty regularly hear people warning of “lifestyle creep.” Sure, spending less is good if it’s in service of some other goal such as retiring early or lowering risk. But spending less shouldn’t be it’s own goal. I’m not saying spending for the sake of spending is the right move, but the more you’re able to spend on the things that matter to you, the better. That could be family vacations, your kids’ college, hobbies, charity, whatever.

It’s worth noting that while retirement age is well-defined, spending is not. How much one spends is a value that changes over the course of their life. However, it’s not actually important that we can place a single number to this, but that different outcomes can be ordered or compared by preference. Presumably, a computational tool like Syrplus could achieve something similar by formulating some proxy for the desirability of different spending styles. Although it’s not as easy as using sum total lifetime spend since the way to maximize this is almost certainly to spend very little for all of one’s life (instead investing and growing one’s accounts as large as possible) and then rapidly spend it all at the end of one’s life.